French Imports of Urea Are Rising Quickly Before Changes to Carbon Regulations (Cbam): A Case Study From Late 2025 to Early 2026

: A Case Study From Late 2025 to Early 2026")

- Mar 13, 2026

French Imports of Urea Are Rising Quickly Before Changes to Carbon Regulations (Cbam): A Case Study From Late 2025 to Early 2026

France acquired a lot more urea in the second half of 2025. There was a huge surge in December that many people felt was because they were buying ahead of the EU's Carbon Border Adjustment Mechanism (CBAM) compliance phase starting on January 1, 2026.

The Plot in One Line

As per France Import Data by Import Globals, this case indicates that climate change-based trade policies can influence the flow of commodities even before the first euro of carbon price is paid.

Urea is not only a "fertilizer." It is an important resource for European farming, an industrial chemical feedstock, and AdBlue/DEF (diesel exhaust fluid) helps cut down on pollution from traffic. Importers have a strong motivation to buy sooner, make sure they have enough, and keep track of the paperwork when they realize that expenses are going up and there will be more paperwork. The rise in late 2025 in France teaches dealers, manufacturers, logistics workers, and compliance teams across Europe's carbon-exposed supply chains important lessons.

Why Policy Changes Affect Urea So Much

Urea is at the crossroads of pollution from industry, food security, and energy costs:

- Urea is a main nitrogen fertilizer that farmers use. As per France Export Data by Import Globals, prices and how simple it is to find something can also vary demand, along with the seasons and the weather.

- Resins and other chemicals are made with urea. It is also a key ingredient in diesel exhaust fluid, which helps huge buses and vehicles cut down on NOx emissions.

- Making urea releases a lot of carbon because it uses a lot of ammonia, which is usually manufactured from natural gas or other fossil fuels. This means that it has a lot of emissions built in.

- When the EU makes it mandatory for importers to disclose and eventually pay for embedded carbon emissions, the economics and timing of urea imports became more problematic. As per France Import Export Trade Data by Import Globals, even if the prices start out slowly, the paperwork and verification procedures might still affect whether or not people buy.

What Changed Exactly: Cbam Goes From "Reporting Mode" to "Compliance Mode."

CBAM has been Coming out in Stages:

- Transitional phase (reporting only): Importers must disclose embedded emissions for covered commodities, building systems, and data pipelines.

- Definitive/compliance phase (starting January 1, 2026): CBAM moves on to its next step. As per France Import Custom Data by Import Globals, importers must follow the definitive regime requirements and get ready for certificate responsibilities on covered items, including fertilizers.

Companies don't like uncertainty, so the market starts to feel the effects even before the first compliance deadlines hit. When you bring in a carbon-heavy commodity like urea, you have to think about a lot of things:

- Will my supplier give me verified emissions data on time?

- Will the paperwork for customs match the CBAM report?

- Will the default emissions values be used (which are often worse than the real ones)?

- How much will I have to pay once certificate surrender starts to rise?

In 2025, a lot of purchasers chose a straightforward solution: buy more and buy earlier, when the regulations were clearer (the reporting phase was known) and before it become harder to follow the requirements.

The Late-2025 Surge: what happened in France

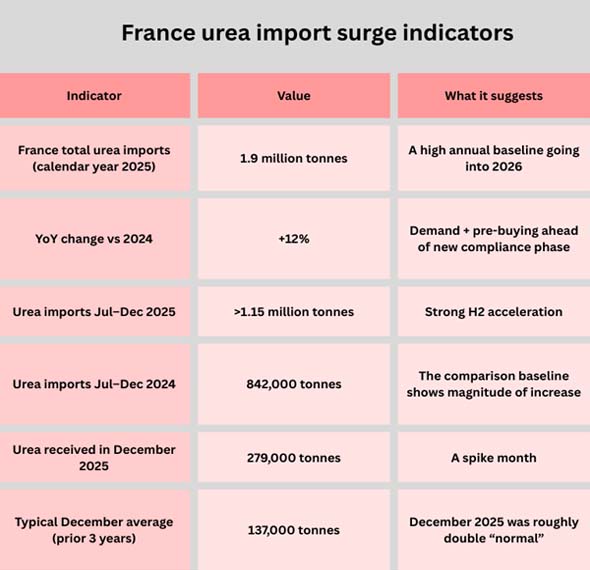

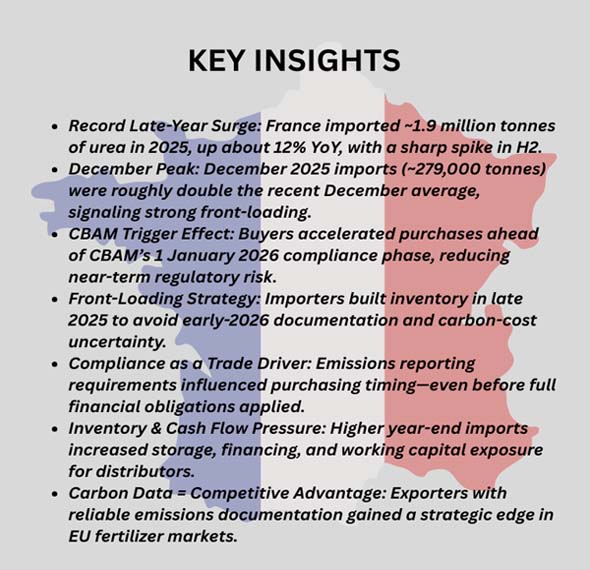

In the calendar year 2025, France brought in over 1.9 million tons of urea. As per France Import Trade Analysis by Import Globals, this was roughly 12% more than in 2024 and much above the current multi-year norm. The most noticeable pattern was the speed up from July to December 2025, when volumes rose sharply compared to the same time in 2024. December 2025 was a peak month, far higher than normal December values.

This conduct fits with the usual "policy pull-forward" pattern: when a new compliance burden is coming up, buyers stock up on goods ahead of time to lower their short-term risk and exposure.

It's not enough to say that "imports rose." Timing is the most important thing to remember. France didn't just buy more urea during the year; it bought more in the months right before CBAM's 2026 compliance phase.

Why Consumers Sped Up: The Reasons Behind the Hurry

There are a few practical reasons for the rise in late 2025. CBAM was the spark, but the market's reaction was complicated.

1) Uncertainty A France Exporter Data

As per France Exporter Data by Import Globals, importers need to know how much pollution is caused by the things they import under CBAM. That means for fertilizers:

- Getting information on emissions from companies outside the EU

- Putting items in the right CN codes (urea is CN 3102 10 and its sub-codes)

- Making sure that customs declarations and CBAM reports match up

- Getting ready for situations where verified data isn't available and default values are used.

In commodity markets, compliance friction can cost as much as tariffs because it slows down clearing, raises working capital, and puts companies at risk of fines. A lot of customers think of pre-buying as "compliance insurance."

2) Expectations for Prices: "Shadow Pricing" for Carbon Costs Starts Early

As per France Importer Data by Import Globals, even if the financial requirements grow over time, people in the market start to think about carbon-linked prices. In real life, a shadow carbon price can show up in deals and negotiations:

- Sellers may add risk premiums to CIF/DEL offers.

- Before the market becomes more unclear, buyers may try to lock in volumes.

- Traders might move sooner to get storage and distribution spaces.

3) Security of Supply: Making Sure There Are No Delays During the Regulatory Cutover

Shipping timetables for the end of the year are already limited by things like bad weather, holidays, and busy ports. You acquire a second layer of bottleneck risk when you add policy change:

- A lot of packages might fill up freight space quickly.

- During "new rules" transitions, mistakes in paperwork are more common.

- If officials do more checks, it can take longer for customs to clear goods.

- So purchasers hurry not only to reduce carbon exposure, but also to avoid problems with logistics and clearance.

4) Strategic Inventory: Fertilizer is Only Needed at Certain Times of the Year, but Compliance is Always Needed

As per France Import Shipment Data by Import Globals, demand for fertilizer changes with the seasons, but compliance obligations do not. Importers would rather construct a buffer so they can keep shipping until early 2026, when compliance processes settle down. For big agricultural importers and wholesalers, having inventories onshore is useful for business.

What this Means for Eu Markets in 2026: What Happens When You Front-Load

Front-loading impacts the way the market works heading into the next year. It can change how demand looks and cause prices to act in ways that are not expected.

1) Ask for "Air Pockets" After a Spike

If demand for the second half of 2025 was moved up, imports in early 2026 would look weaker than they would have been otherwise since buyers had already filled their storage. That can make things soft in the near term, even if consumption stays the same.

2) Stress from Storage and Finance

There are expenses to building inventory:

- Availability of storage and terminal fees

- Needs for working capital

- Credit and trade finance constraints

There is a danger of losing money on inventory if prices go against the customer. Big companies might find this easy to deal with, but smaller importers might have a hard time, which could mean that bigger companies get more market share.

3) More Attention Paid to Where Things Come From and How They Are Classified

As CBAM compliance grows, customs and regulators pay more attention to:

- Correct CN categorization (this is especially crucial for fertilizer sub-codes)

- The stated producer and installation information (if needed)

- Shipping documents and CBAM reports should match up

- Possible circumvention behaviors (such misclassifying or routing games)

- "Clean paperwork" gives importers an edge over their competitors.

What Exporters and Producers Should Learn From the Global Ripple Effect

The rise in urea prices in France in 2025 is a warning and an opportunity for suppliers outside the EU.

1) Emissions Data is Now a Feature of Products That Are Sent to the EU.

As per France Import Export Trade Analysis by Import Globals, in the CBAM era, your urea isn't just a chemical; it's a package that comprises

- A profile of carbon

- Quality of the documentation

- Ready for verification

- The capacity to answer queries from importers rapidly

Even if their headline price is a little higher, producers who can provide reliable emissions data and dependable documentation will gain market share.

2) "Cleaner" Means of Making Things Might Give Businesses an Edge

Over time, ammonia routes that produce fewer emissions (including renewable-based pathways when possible) could cut embedded emissions and, as a result, the cost of CBAM. Not every exporter can change course rapidly, but it's evident that carbon intensity is becoming a factor in competition.

3) Traders Will Change the Price of Risk, and Contracts Will Change

Expect to see more contract conditions that have to do with reporting emissions and default settings. Who is in charge of making sure the data is correct and audits are done? Changes in Incoterms preferences based on who can handle compliance.

A Practical Guide for Businesses on How to Respond in 2026

This case study provides a definitive checklist for companies importing CBAM-regulated products such as fertilizers:

Map the CN Codes and the Range of Products

As per France Export Import Global Trade Data by Import Globals, make sure that the classification of products is correct and stays the same in both customs and internal systems.

Make a Conduit for Emissions Data

Get emissions data from suppliers, check it, store it, and connect it to shipments and customs reports.

Think About the Risk of "Default Values"

If you can't get verified data, model the worst-case exposure and utilize it in discussions for purchase.

Plan Logistics and Make Sure They Are Legal

Don't think about CBAM as an afterthought. Shipping papers, customs forms, and reports on emissions must all be the same.

Make Supplier Governance Stronger

Choose providers who can always offer paperwork and proof, especially when enforcement is still new.

Conclusion

The rise in urea imports to France in late 2025 is a perfect example of how markets react when rules go into effect. As CBAM moved into its 2026 compliance phase, purchasers moved volumes ahead, which led to higher imports in the second half of the year, a spike in receipts in December, and a change in the inventory picture going into 2026.

The lesson for the trade community as a whole is simple: carbon control is no longer a distant policy idea; it is now a supply-chain variable. It changes when you buy things, how you document them, how you pay for them, when you ship them, and who you choose as your supplier. Companies that approach compliance readiness as part of cost, quality, and reliability will have the edge in 2026. This is because it is becoming more and more important. Import Globals is a leading data provider of France Import Export Trade Data.

FAQs

Que. What caused French urea imports to skyrocket in late 2025?

Ans. A lot of buyers bought things faster before CBAM's compliance phase in 2026 to lower their risk of regulatory and documentation issues in the short future and make sure they had enough supply.

Que. Is CBAM already charging importers as of January 1, 2026?

Ans. After the transitional reporting period, CBAM will enter its final/compliance phase on January 1, 2026. The definitive regime framework includes financial duties and processes.

Que. Does CBAM include fertilizers like urea?

Ans. Yes, CBAM does encompass fertilizers, and urea is among the CN classification family that CBAM uses in its scope and methodology publications.

Que. What should urea exporters to the EU do in 2026?

Ans. Get ready for reliable emissions records, verification-ready data, and consistent shipping and customs paperwork. This is because the quality of carbon data is becoming a business need.

Que. Where to get detailed France Import Export Global Data?

Ans. Visit www.importglobals.com.